At its event next week, the Federal Reserve is forecast to raise the FFTR by 50 bps, comments Economist at UOB Group Lee Sue Ann.

50bps each in the Jun and July FOMC

“Given the clear indications for ongoing hikes to combat inflation spelt out in the May FOMC minutes but no intentions of cranking up the size of the hikes, we are comfortable to maintain our FFTR forecast for another 50bps each in the Jun and July FOMC.”

“We continue to expect 25bps in every remaining meeting of this year. This will bring the FFTR higher to the range of 2.50- 2.75% by end of 2022, a range largely viewed as the range for neutral stance.”

- The ECB is set to announce the end of its QE program and signal a rate hike in July.

- Without indicating a double-dose increase to borrowing costs, the euro could fall.

- Elevated inflation forecasts are likely to fail in lifting the euro if growth projections are downgraded.

Inflation is here

The ECB last increased borrowing costs in 2011, when higher prices pushed inflation beyond its “2% or close to 2%” target, and then-President Jean-Claude Trichet decided to act with “strong vigilance.” It was a total disaster. The eurozone entered a second recession and policymakers have since had to invent new tools to prevent deflation.

Eleven years on, and the world has materially changed. Headline eurozone inflation has hit 8.1% YoY in May, similar to US levels. And while Russia-related energy prices and supply-chain issues are responsible for most of these gains, core prices are also rising in the old continent. These reached 3.8% yearly in May.

Let us see what scenarios we can expect.

1) The unlikely instant hike

Despite the narrow window to act, the ECB’s insistence on communication consistency means it is only expected to announce the end of bond-buying in July, and pre-announce a rate hike in its upcoming meeting, also next month.

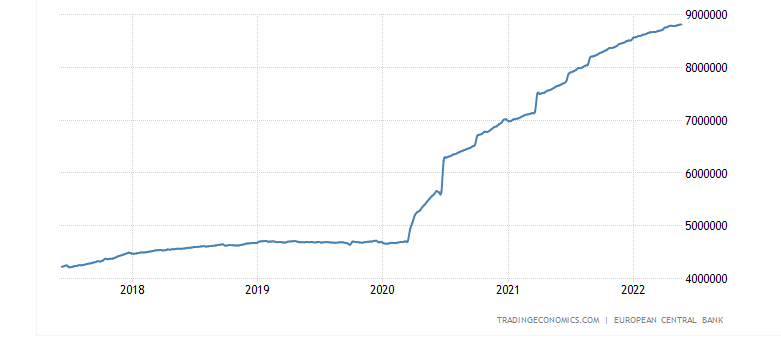

The ECB’s balance sheet is at nearly €9 trillion:

Source: Trading Economics

There is a low chance that the hawks will convince ECB President Christine Lagarde and other doves to hasten the process and raise interest rates now. In that highly unlikely scenario, EUR/USD would surge instantly on the shock move, but it could also fall as quickly. As our recent experience with the RBA has shown,

if investors see such a quick move as mere front-loading of future moves – and even as “higher rates now, lower in the long run” – any EUR/USD rally would be short-lived. It would even turn into a selling opportunity.

2) The highly likely 25 bps signal for July

ECB President Lagarde seemed to have ditched her abstract language in recent months, opting instead for clearer messages. Her preferred move is to raise rates by 25 bps in July and then another such move in September, bringing the deposit rate to 0%. Later on, she foresees further increases – but that will have to wait for its due time.

If she indeed reiterates that message, this time in an official rate-setting environment and also based on discussions and forecasts, I expect EUR/USD to decline. That would be a “buy the rumor, sell the fact” response. The common currency’s price has such moves fully baked in.

The ECB deposit rate is in deeply negative territory:

3) Open door to 50 bps moves

Another scenario that cannot be ruled out is that Lagarde leaves the door open to 50 bps hikes, even as soon as July. Such an outcome could be the result of fresh forecasts compiled after the most recent inflation data. If Lagarde says such an option is on the cards and depends on data, the euro would have room to rise.

In turn, a stronger exchange rate would also help depress the costs of imported goods, thus helping to reduce inflation. Moreover, uncertainty about how much the ECB could do in July and beyond would also add to the speculation, further boosting the euro after the dust settles on the ECB decision.

4) Open door and no floor ahead

One caveat about an open-door policy is the ECB’s forecasts. Several officials have signaled that GDP growth projections could be slashed in the upcoming meeting, as a result of the war, China’s covid-related lockdowns, and uncertainty about the scope of the recovery.

If the ECB says it will either raise by 25 bps or by 50 bps but cut its growth expectations, investors are likely to err on the side of downbeat projections. If the eurozone is set to expand at a slower rate, so is inflation – reducing pressure on the ECB to act.

In such a scenario, EUR/USD would likely end the day lower, as the currency aligns itself with gloomier forecasts rather than with hope for hawkish policy.

Final thoughts

The ECB will most likely opt for what it already signaled – a 25 bps hike in July. Communication consistency means “buy the rumor, sell the fact.” However, other scenarios cannot be ruled out. The world is moving much faster and even the old continent adapts to shifting sands.

सोशल मीडिया अपडेट्स के लिए हमें

Facebook ( https://www.facebook.com/goldsilverreports/ )

linkedin (https://www.linkedin.com/in/nealbhai/ )

और Twitter ( https://twitter.com/goldsilverrepor ) पर फॉलो करें।

हमारी फ्री सर्विस और लोगो की paid सर्विस से कई गुना अच्छी है।

आपको हर दिन दिए जाएंगे 3 से 5 कॉल बिलकुल फ्री

हर CALL में PROFIT दिये जायेंगे

तो जल्दी से MCX CHANNEL को JOIN कर लो (NEAL BHAI REPORTS)

JOIN US CLICK HERE

EQUITY CHANNEL को JOIN कर लो (EQUITY FREE TIPS)

JOIN US CLICK HERE

US dollar retreats as market sentiment dwindle ahead of key inflation data, Treasury yields grind near monthly top.

Gold Price is testing bearish commitments at the key $1,837 support.

ECB couldn’t impress gold buyers:

The European Central Bank (ECB) signaled that the fears of inflation challenge the old continent’s growth, via the economic forecasts. The bloc’s central bank also matched market consensus while announcing an end of Quantitative Easing from July 1 and 25 basis points (bps) of a rate hike on July 25. However, the market’s expectations of a 50 bps move in July were pushed back and hence drowned the gold prices after the ECB announcements.

सोने की कीमत मजबूत ट्रेजरी बांड प्रतिफल का बोझ वहन करती है

तीन-दिवसीय अपट्रेंड के दौरान यूएस 10-वर्षीय ट्रेजरी बॉन्ड यील्ड 1.7 बेसिस पॉइंट (बीपीएस) बढ़कर 3.057% हो गया। ऐसा करने पर, बेंचमार्क बॉन्ड कूपन दूसरे साप्ताहिक लाभ के लिए तैयार होते हैं, जबकि पिछले दिन मासिक शीर्ष पर पहुंच जाते हैं। आक्रामक केंद्रीय बैंक कार्रवाइयों की आशंकाओं को हाल ही में बांड यी में रन-अप से जोड़ा जा सकता है