Most Asian stocks slipped Tuesday amid caution over economic risks from the omicron virus strain as well as central bank efforts to rein in elevated inflation. Treasuries and the dollar held gains.

MSCI Inc.’s Asia-Pacific share index fell for a third session, with Chinese technology stocks struggling. Concerns about China’s property sector have also flared anew, and the real-estate downturn likely contributed to a slowdown in the nation’s economic activity in November.

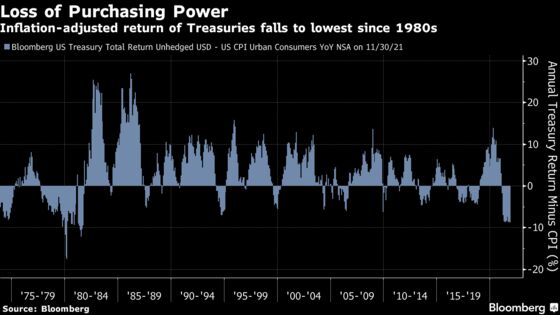

Technology Heavy Nasdaq 100 Underperformed

U.S. and European equity contracts edged higher. The S&P 500 on Monday dropped from a record and the technology-heavy Nasdaq 100 underperformed.

Treasury yields declined in U.S. hours in the mood of risk aversion, led by the 30-year bond. Traders are braced for the Federal Reserve to taper stimulus more quickly and signal an interest-rate liftoff in 2022, both potential economic challenges. The Fed policy decision due Wednesday is among 20 central bank meetings this week that could stir market swings.

Investors are continuing to grapple with the implications of reduced central bank support and are awaiting more clarity on the economic threats from omicron.

“Volatility will remain elevated throughout all of this week’s rate decisions from the Fed, ECB and BOE,” Edward Moya, senior market analyst at Oanda Corp., wrote in a note. “2022 is still expected to be a strong global growth story, but accelerated central bank hawkishness could be the one thing that helps deliver the first major pullback with U.S. equities.”

In commodities, crude oil held a retreat in part on the possible obstacles to global reopening if omicron leads to wider mobility curbs. Bitcoin extended its tumble from a November all-time high to more than 30%.

“It has been a strong year, we expect it to end strong, but investors have to be careful with bubble assets,” Eva Ados, ERShares chief investment strategist, said on Bloomberg Television. “The worst when it comes to inflation is behind us. Tapering has been somehow baked in. We are cautiously optimistic, but there are many risks on the horizon too.”

On the virus front, the omicron variant dented the protection afforded by two doses of Pfizer Inc.’s and AstraZeneca Plc’s Covid vaccines as feared, researchers found, increasing the risk of infection. China reported its first omicron case.

Goldman Sachs Group Inc. told its London staff to work from home if they can, and Fidelity Investments paused its voluntary return-to-office pilot program in New England. The U.S. topped 50 million cases of Covid-19.

Here are some key events this week:

- Euro zone industrial production, Tuesday.

- U.S. PPI, Tuesday.

- China releases November industrial output, retail sales data, Wednesday.

- Fed rate decision, Wednesday.

- U.S. business inventories, retail sales, empire manufacturing, Wednesday.

- BOE rate decision, Thursday.

- ECB rate decision, Thursday.

- U.S. housing starts, initial jobless claims, industrial production, Thursday.

- BOJ monetary policy decision, Friday.

- S&P Dow Jones Indices quarterly rebalance effective after markets close, Friday.

- “Quadruple witching” day in the U.S. market, when options and futures on indexes and equities expire, Friday.

For more market analysis, read our MLIV blog.

Some of the main moves in markets:

Stocks

- S&P 500 futures rose 0.1% as of 10:50 a.m. in Tokyo. The S&P 500 fell 0.9%

- Nasdaq 100 futures rose 0.1%. The Nasdaq 100 fell 1.5%

- Japan’s Topix index rose 0.1%

- Australia’s S&P/ASX 200 Index fell 0.3%

- South Korea’s Kospi index fell 0.2%

- Hong Kong’s Hang Seng Index index fell 0.9%

- China’s Shanghai Composite index fell 0.4%

Currencies

- The Japanese yen was at 113.63 per dollar

- The offshore yuan was at 6.3697 per dollar

- The Bloomberg Dollar Spot Index was little changed

- The euro was at $1.1280

Bonds

- The yield on 10-year Treasuries was at 1.42%

- Australia’s 10-year bond yield fell six basis points to 1.54%

Commodities

- West Texas Intermediate crude was at $71.21 a barrel

- Gold was at $1,787.64 an ounce

Comments are closed.